Household and Housing Debt reach new record highs

Each quarter the Reserve Bank (RBA) releases its selected ratios of household finances. The latest data for December 2015 shows the ratio of household and housing debt to disposable income has continued to climb.

The latest ratios of household finances highlight that the ratio of debt to disposable income is at a record high however, the value of household assets is also at a record high level. Meanwhile with record low interest rates, the ratio of interest payments to disposable income is the lowest it has been since early 2003.

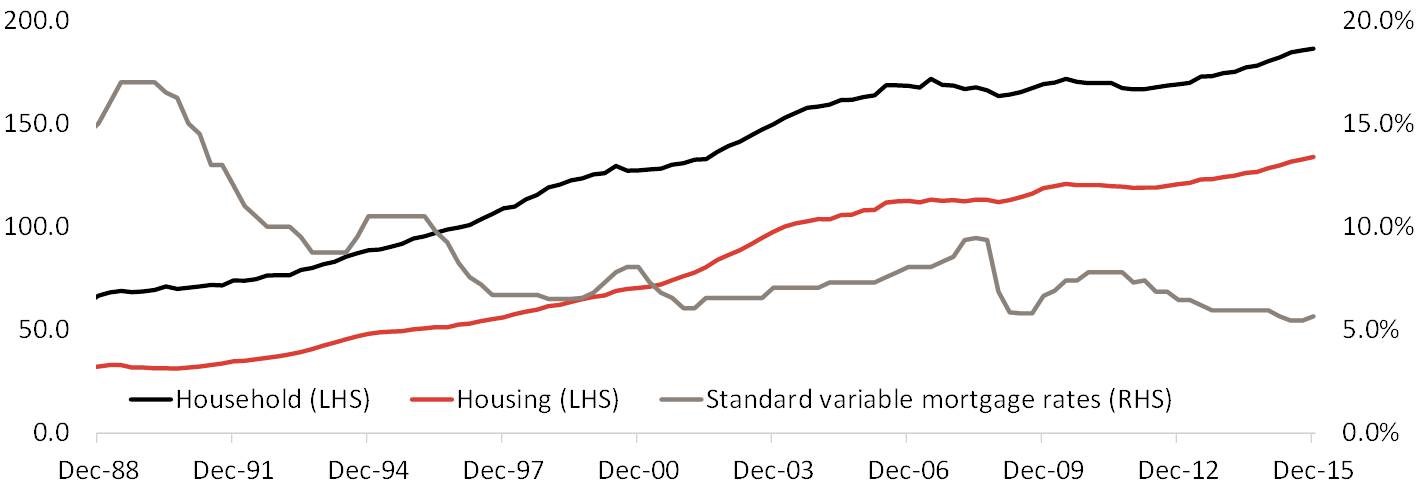

The first chart highlights the ratios of housing and household debt to disposable incomes and plots it against standard variable mortgage rates. The ratio of household and housing debt to disposable incomes are each at historic highs of 186.3% and 133.8% respectively with the ratios increasing by 3.4% and 4.3% over the past year. Over the period from 1988 to 2015 standard variable mortgage rates have fallen dramatically and that has surely contributed to household’s preparedness to take on more debt.

Ratio of household and housing debt to disposable income

vs. standard variable mortgage rates

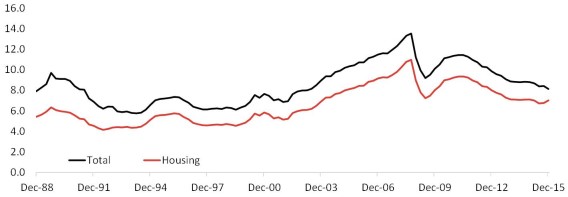

To further highlight this point, the second chart looks at the ratio of household and housing interest payment to disposable incomes. Over recent years the ratio has been falling with the ratios for households and housing sitting at their lowest levels since 2003. The higher ratio of interest payments currently compare to 1988 when interest rates were substantially higher is reflective of the much higher cost for household assets, particularly the cost of residential housing.

Ratio of household and housing interest payments to disposable income

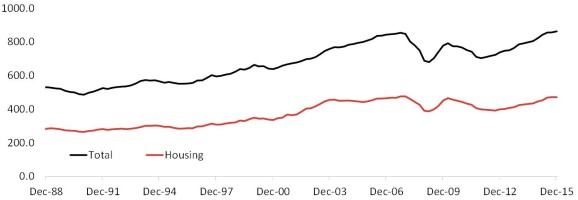

Although households have significant debt, particularly for housing, the value of the assets they hold is substantial. The ratio of household debt to disposable income is currently 186.3% however, the ratio of household assets to disposable income 862.8%, the highest it has ever been. Similarly, the ratio of housing debt to disposable income is 133.8% however, the ratio of housing assets to disposable income is 471.3%. Interestingly, the ratio of household assets to disposable income is still lower than its previous peak in December 2007 at 476.2% but it is nudging back up towards its previous record high.

Ratio of household and housing assets to disposable income

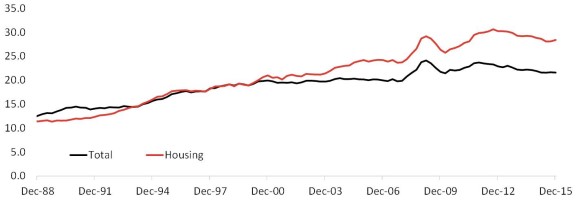

The value of households’ assets are significantly greater than the value of the debt and this is highlighted in the fourth chart. Based on this data, the ratio of household debt to assets is 21.6% and the ratio of housing debt to housing assets is 28.4%. The chart also shows that the ratios have been trending lower recently although the housing assets to debt ratio increased slightly over the December 2015 quarter due to weaker home price growth.

Ratio of household and housing debt to assets

Australian households are heavily indebted, with most of this debt due to residential housing. While the debt is high, the value of the assets held is much greater than the debt. A few things which are important to consider however, are that this is a national view and across different regions the ratios are likely to be substantially different. Furthermore, lower interest rates and a fairly strong labour market over recent decades has contributed to Australian’s preparedness to borrow. Were either of these factors to change it could lead to a dramatic deterioration in the value of these assets while of course the debt would remain. Importantly, mortgage arrears remain low and the Reserve Bank has reported that the typical mortgage holder is currently more than two years ahead on their mortgage repayments. This coupled with higher rates of household savings provide a potential buffer if unemployment were to rise sharply or interest rates began to increase.

Source: CoreLogic by Cameron Kusher